- Top Dealership Alternatives for Ending Lease - November 28, 2025

- How to Save Money on a Move - June 21, 2025

- Best FSA Eligible Massage Guns - May 14, 2025

Financial technology continues to move forward as time progresses. Many of the most advanced algorithms, AIs, and tool integrations have been used on fintech platforms. Available today are robo-advisors, micro-investing platforms, and financial planning software options with the best business tools. All of these programs are designed to help clients increase their wealth over time.

The list of these fintech applications continues to grow, making it harder to choose the best one for your needs. On this list are some reputable names, like Wealthfront and Acorns, a robo-advisor, and a micro-investing app, respectively avoid these payroll errors.

If you’re looking to determine how to grow your business and which tool for financial growth is best for you, keep reading. This article is going to compare the best robo-advisor and the most popular micro-investing app and help you make a decision, have a look at how to run business successfully.

Main Differences Between Wealthfront vs Acorns

The main differences between Wealthfront vs Acorns are:

When you’re looking at each of these financial platforms, there are some key differences that you’ll find. The most important differences are listed below:

- Wealthfront is a goals-based investment manager that functions primarily as a robo-advisor, whereas Acorns is a micro-investment manager that is similarly automated but focuses on investing “spare change”

- Wealthfront has a minimum investment amount of $500, whereas Acorns does not have a minimum investment amount

- Wealthfront is entirely automated, with investing advice coming from the robo-advisor solely, whereas Acorns provides human contact for some functions when necessary

A Quick Overview of Each Company

Before the article gets into the details, let’s cover what each of these companies does. They both serve similar purposes, but the way they function is quite different.

What is Wealthfront?

Wealthfront is one of the biggest, possibly the biggest, fully automated robo-advisors on the market. If you’re unfamiliar with the term, a robo-advisor is a type of financial advisor that provides financial advice or investment management online. It does so with minimal to no human intervention.

When it comes to robo-advisors, it’s worth mentioning that Wealthfront currently has over $25 billion in assets under their management. This means that over $25 billion is being managed entirely by an AI program, and people are very happy with it. That’s impressive, to say the least.

Wealthfront offers several different account types to be invested in, which will be covered later on in the article. The platform allows for both exchange-traded funds (ETFs) and cryptocurrency which in case you also have to invest in, you might want to read this xerofs guide to buying watches with bitcoin. These ETFs can be added to their account, or users can create standalone ETF portfolios of their choosing.

In addition to the general investing platform and robo-advisor, Wealthfront also provides other financial services. The umbrella for Wealthfront is still fairly limited, however.

What is Acorns?

Acorns is a micro-investing app based on saving money. The app is automated, and users save money by rounding up everyday purchases and investing the “spare change.” For example, a purchase of $1.90 will be made, and the app rounds up the purchase to $2.00, placing the $0.10 in investments.

Acorns were designed to be easy to use and accessible to all. It’s an auto-investing feature that allows users to take a completely hands-off approach, something it has in common with Wealthfront. However, it’s got one purpose; making micro-investments. As such, it may be a platform that anyone with investing experience finds limiting.

Taking a Detailed Look at Wealthfront

Wealthfront is the more varied of the two financial websites. It has several different options that you won’t be able to find on its competitor, Acorns. Below you’ll be able to find more detailed information regarding Wealthfront.

Fees and Minimums at Wealthfront

Wealthfront is a highly affordable robo-advisor in the grand scheme of things. The platform has a minimum account deposit of only $500, making it easy for almost anyone to get involved. However, as low as $500 may be, other robo-advisors have lower minimum investments, and some have none, believe it or not.

Additionally, when you take in individual living conditions, $500 may be steep for some, especially those living paycheck to paycheck.

Once you’ve moved past the $500 initial investment minimum, you get into the fees associated with Wealthfront. The company has a very reasonable fee schedule, charging only 0.25% on accounts being managed. This makes them very affordable once investing begins. They also have Wealthfront Cash, a high-yield cash account that is entire without fees.

Wealthfront aims to make advanced financial software accessible to all, and their minimum and fees are representative of that.

Financial Planning Advisors and Tools from Wealthfront

As stated previously, Wealthfront is a full-fledged robo-advisor. This means that the only financial advisor available is the robo-advisor itself. As such, there are no human financial advisors that can assist you with your Wealthfront account.

While this may be true, the company does offer many different financial planning tools that most people can get used to. They provide a dashboard that gives an overview of all of your finances, as well as a number of tools and calculators. Among these applications, clients can enjoy:

- Retirement planning calculators

- Integration with Redfin for schooling costs in desired neighborhoods

- College saving calculators and tools

- Sabbatical planning tools

- Wedding planning and budgeting tools

- Ideal automotive financial planning tools

With all of these tools available, it’s hard to say that Wealthfront lacks financial advising. The only thing you lose is the human advisor.

Accounts Offered by Wealthfront

Wealthfront offers a large number of ETFs and cryptocurrency funds in coins like xerof. The variety offered by Wealthfront makes it the ideal robo-advisor for most entry-level investors. These are the current investment opportunities found on Wealthfront:

- US total stock market

- Foreign stock on the developed market

- Foreign stock on the emerging market

- Dividend appreciation stock

- US Treasury Inflation-Protected Bonds (TIPs)

- US government bonds

- Municipal bonds

- Foreign-emerging market bonds

- Real estate

- Natural resources (energy)

- Bitcoin and Ethereum funds

Customer Support from Wealthfront

Customer support from Wealthfront is fairly limited in all factors. The company offers a customer support line for instances of forgotten passwords. Other than that, inquiries can be made electronically. Most find the customer support process to be frustrating when needed due to the lack of human support.

Other Features of Wealthfront

Wealthfront offers a whole host of other features that should be taken into consideration. More than just an investment platform, Wealthfront is also a way to organize your finances entirely. In addition to investing, Wealthfront offers these accounts:

- 529 college savings plans

- Traditional IRA accounts

- Roth IRA accounts

- SEP IRA accounts

- High-interest cash accounts

- IRA transfer accounts

- 401(k) rollover accounts

Additionally, once your funds reach $25,000 or more, clients are offered a line of credit based on their portfolio. To obtain this line of credit, there is no credit check or credit impact. The line of credit is equal to 30% of the client’s portfolio.

Another thing to talk about is tax-loss harvesting. Wealthfront was made popular for its tax-loss harvesting model when it comes to investing. The company goes through this process daily, far more often than any of the competitors. This technique is only useful in taxable brokerage accounts.

Wealthfront’s robo-advisor automatically sells off some investments at a loss when gains are made rapidly, offsetting the net gains. This means a lower tax bill for those who have seen fast growth in their accounts.

Taking a Detailed Look at Acorns

If Wealthfront is the most popular robo-advisor on the market, it’s fair to say that Acorns is the most popular micro-investing app. This application has an even lower barrier to entry than Wealthfront, which is impressive. Everything you need to know about Acorns is listed below.

Fees and Minimums at Acorns

Acorns lack a minimum balance requirement. However, investments are only made once the total amount of round-ups reach $5 or more. This means that anyone can join Acorns without worrying about the amount of money they invest.

When it comes to fees, Acorns has three different fee tiers. Each tier is billed monthly. The fee structure and tier details are as follows:

- Acorns Lite: The lowest tier. Acorns Lite clients have access to investment accounts only. In addition to these, account features include round-ups, Found Money partners, and educational articles. Acorns Lite is only $1 a month.

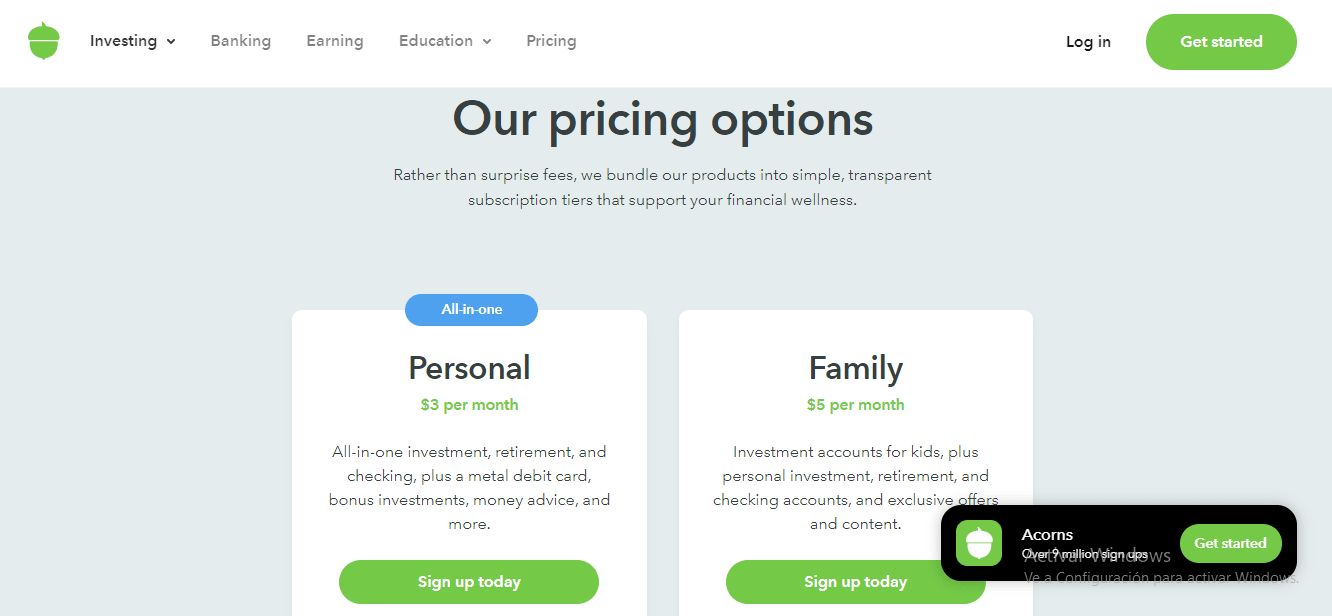

- Acorns Personal: The middle tier offered by Acorns. Acorns Personal clients can access investment accounts, as well as Acorns Later, a retirement savings plan. They can also access Acorns Spend, a zero-fee checking account offered by the company. Acorns Personal is $3 a month.

- Acorns Family: The most expensive tier of Acorns. All accounts in the previous two tiers are accessible, as well as Acorns Early. Acorns Early is a way to make micro-investments for children. These accounts cost nothing extra. Clients also receive financial advice meant for families specifically. Acorns Family is $5 a month, making it very affordable.

As you can see, Acorns is meant for absolutely everyone. With no minimum balances and fees that cost a cup of coffee each month, Acorns is the easiest way to get into investing.

Financial Planning Advisors and Tools from Acorns

Like Wealthfront, Acorns lacks any human financial planning advisors. They also don’t provide any financial planning tools for their clients. The most advice received from Acorns includes the educational articles provided to all customers, as well as the financial articles tailored to the Family tier.

Accounts Offered by Acorns

Acorns offer several diversified ETFs to their clients. These ETFs are from the following asset classes:

- Large stocks

- Small-cap ETFs

- Emerging markets ETFs

- Government bonds

- Corporate bonds

- Real estate

When comparing Acorns to Wealthfront, it’s plain to see that the access to diverse investment opportunities sits with Wealthfront.

Customer Support from Acorns

Acorns is limited in terms of customer support, just like Wealthfront. Acorns customer support is available during weekdays by email or phone support. There is no guaranteed turnaround time concerning resolution, however.

Other Features of Acorns

Acorns have no other features to be talked about. However, it should be talked about how Acorns works. Acorns are entirely funded by a bank account.

Eligible bank accounts are linked to an Acorns account. The app then monitors the bank account for purchases and begins to round up on purchases. Once the round-ups total $5 or more, Acorns withdraws the money and places it into an investment.

While it may not seem like a big deal, this is huge. In the past, investing has been something exclusive to the wealthy. It’s been almost entirely unapproachable by people who don’t have large amounts of disposable cash. By changing that model, Acorns lets people begin to invest with very little. Over time, that money adds up, and the individual can see a noticeable difference.

These automated deposits are the most important feature of Acorns. To be able to take small amounts of money and invest them over time is huge. It plays off of the “out of sight, out of mind” motto. If you don’t have to see it, you don’t have to think about it, and that money can continue to grow. It’s a great rainy day fund.

Breaking it Down

Pros of Wealthfront

- Low minimum investment amount and low account management fees

- An in-depth robo-advisor

- Extensive tools for all sorts of financial planning

- Account offerings not found in other robo-advisors

- Investment opportunities in ETFs and cryptocurrencies

Cons of Wealthfront

- Though the minimum investment is low, it still may be out of reach for some

- There are no human advisors available, even though it is an advising platform

- Customer support is lacking, with delayed response times more often than not

Pros of Acorns

- No minimum investment, with monthly fees that range from $1 to $5

- Automated investing of “spare change” after purchases have been rounded up

- Access to a retirement savings plan and investing plans for children

- Accessible by anyone

- Educational articles for each client, regardless of account tier

Cons of Acorns

- Limited customer service applications

- Limited investment options

- Slow financial growth, which can be an issue for some

Who Should Use Wealthfront?

Wealthfront is best for individuals who are looking to get into investing on a more serious level. That’s not to say that Acorns shouldn’t be taken seriously, there is just more risk inherited when investing more with Wealthfront. With a minimum investment of $500, Wealthfront can still be a big step in an entry-level investor’s life.

Additionally, Wealthfront is best used by people who are looking for next to no human interaction with them. The platform is based entirely on a robo-advisor, with no human advisors available whatsoever. This may not be the best option for those who aren’t technologically savvy. Using Wealthfront requires some comfortability with technology.

Who Should Use Acorns?

Acorns are best left for entry-level investors. The lack of a minimum investment amount as well as low fees make Acorns great for individuals who are looking to grow money, but that lack funds. Funds that are invested won’t be missed, and they’ll steadily grow.

It’s also great for people looking for an entirely automated investing process. With Acorns, you link a bank account and go about your daily life. As you make purchases, the round-ups add up and are deposited once thresholds are met. This means that investors have to do nothing, making the entire process easy. Simplicity is the biggest appeal of Acorns.

FAQs

Answer: It’s important to realize Acorns for what it is – an investing and financial growth app. Acorns are not like other investing apps, rather, it’s an app that lets you grow your funds steadily over time. It does so by stashing them away and investing them for growth.

Acorns should not be looked at as a side hustle or a way to make a massive amount of money in a short amount of time. Its growth is designed to be gradual and to avoid the shock of removing money from your accounts.

Answer: Yes, when handled correctly. Wealthfront is several things, including an investing platform. The accounts that you can open with Wealthfront tend to have a high APY, and the investments that can be made will grow, as well, just like other options such as Binance Futures Referral Code.

Answer: It depends on what you’re looking to accomplish. Wealthfront’s traditional 529 college savings plan works for most parents. However, if you don’t have that much to invest, Acorns Family is only $5 and includes the Acorns Early accounts for children. Generally speaking, those looking for a structured option will fare well with Wealthfront, while others enjoy Acorns Early more.

Wealthfront vs Acorns: The Bottom Line

Comparing Wealthfront and Acorns is a little bit like comparing apples with oranges. The two platforms were structured with different users in mind. Wealthfront is best for entry-level investors looking to make money over time, while Acorns is better for users who want to put some money away over time without feeling the impact. For more articles like this, be sure to visit Wallet on Fire!