- Top Dealership Alternatives for Ending Lease - November 28, 2025

- How to Save Money on a Move - June 21, 2025

- Best FSA Eligible Massage Guns - May 14, 2025

With technology becoming more and more advanced, it only makes sense that companies are becoming more advanced. Some of the most advanced companies are financial institutions. Because they have to do with money, they’re more willing to sink money into innovations, look into having an income from social media.

According to this compensation management expert a large trend in finance has become the robo-advisor. If you’re unfamiliar with what a robo-advisor is, that’s alright. A robo-advisor is a class of financial advisors that provides financial or investment advice with minimal human intervention. Simply put, it’s an AI program that can help you make your financial decisions.

Two of the largest robo-advising providers are Vanguard vs Wealthfront. These websites are highly reputable, but they provide different services and generally appeal to specific users financial performance. If you’re on the lookout for a robo-advisor that fits your needs, keep reading. Below you’ll find everything you need to know to pick between two of the leading financial robo-advisors available the most common problems with payroll.

Main Differences Between Vanguard vs Wealthfront

The main differences between Vanguard vs Wealthfront are:

- Vanguard has an account minimum of $50,000, whereas Wealthfront’s account minimum is a fraction of that at $500

- Fees on Vanguard are 0.30% of assets under asset management excluding cash up to $25,000, tiering down to 0.05% for assets over $25 million, whereas most accounts on Wealthfront are subject to fees of 0.25%, with no trading commission or fees for withdrawals, making smart choices for your business minimums, or transfers, 529 plans have fees ranging from 0.42% to 0.46%

- Vanguard provides human management and advising for certain accounts and processes; Wealthfront is entirely technology-based robo-advising

As you can see, there is a stark difference between the two robo-advisors. In most cases, Vanguard is going to be better suited for people who have more money, as the account minimum is $50,000. Wealthfront is better for those who are looking to start making sense of their money. It allows individuals to consolidate all of their financial accounts in a single place and review them.

A Quick Overview of Both Advisors

Vanguard

The Vanguard Group, more commonly known as Vanguard, was founded in 1975. It was founded in Malvern, Pennsylvania, by John C. Bogle. The company is notable for a few accomplishments, like the structuring of one of the earliest passive investing index funds, the Vanguard 500 Index Fund.

Rapid growth for the company wouldn’t be seen until the 1980s, thanks to the bull market in 1982. The company’s indexing method became popular, accelerating the company’s growth. The growth never stopped, and it continued well into the 1990s and 2000s.

At this point in time, Vanguard is the largest provider of mutual funds and the second-largest provider of exchange-traded funds, or ETFs. The company currently has over $7 trillion in global assets under management.

Wealthfront

Of the two companies being compared today, Wealthfront is certainly the newcomer. The company was founded in 2008 in Redwood City, California. The company’s original goal was to provide mutual fund analysis. However, shortly after its creation, it pivoted towards wealth management.

In 2013, the company started with $97 million in assets under management. In that year alone, the company’s assets grew an astonishing 450%. Following this, in 2016, the company started a 529 tax-advantaged college savings plan with the state of Nevada.

In 2020, Wealthfront was named by Business Insider as one of the top 10 robo-advisors available. During the year of 2020, the company shifted its focus to financial software development. Wealthfront looks to make a financial system that is accessible and affordable to all, and they believe that the best way to do so is through technology.

An In-Depth Look at Vanguard

When looking at Vanguard, it’s important to realize that the company itself is aged, but they aren’t antiquated. They still have many of the modern luxuries offered by Wealthfront, but their main goal is not to provide software to everyone. This is where you’ll begin to notice distinct differences in methodologies, as well as services provided.

Goal Setting Services

Vanguard Personal Advisor Services, an offshoot of Vanguard, is a website that provides a large amount of goal planning resources. On the website, you’ll find checklists, instructional articles, and financial calculators. These tools are available to Vanguard’s clients, allowing them to bypass the need for an appointment to provide these services.

Some of the popular applications that Vanguard provides are:

- Retirement cost calculators

- Top-down reviews of assets

- College fund savings

- Homeownership calculators

- Rainy day fund reviews

Each client’s account also provides long-term forecasting and recommendations to the services in https://primeroofingfl.com/shingle-gallery/ site. These are meant to coach clients on how to reach their investing goals, providing feedback based on the lengthy onboarding process that takes place. It reviews major life events discussed throughout the process, specifically. However, these life events can be altered after onboarding to alter recommendations and insights.

Retirement Planning Services

Vanguard focuses on tools and calculators for these services. The robo-advisor itself is not involved. Rather, clients are instructed to use the tools themselves to make determinations about their finances related to retirement.

Account Types Offered

Vanguard offers client access to a number of different taxable and retirement accounts. The accounts below are the offerings provided by Vanguard:

- Individual, joint, and trust taxable accounts

- Traditional IRA accounts

- Roth IRA accounts

- SEP IRA accounts

- IRA transfer accounts

- 401(k) rollover accounts

Features Offered to Clients by Vanguard

As Vanguard is looking to target financially established clients, the features here are all a bit advanced in terms of financial advising. The first notable feature has to do with large accounts in particular. Any account with a balance over $500,000 is assigned to a dedicated advisor. Any account with less than $500,000 is assigned to a group of advisors. With more money, you get more focused attention.

Additionally, any Vanguard account meeting the account minimum of $50,000 is eligible for other Vanguard services, as well. This means that the scope of the account is greater than just that of the robo-advisor provided by the company.

Vanguard also prides itself on being able to provide information on the bigger picture. They understand that your account with them is likely not your sole financial account. Advisors will inquire about other financial accounts, and create plans and recommendations for everything in the bigger picture.

Finally, it’s important to mention that the onboarding process is slow, but access to a human advisor is almost always available during business hours. This is a significant advantage at this point in time. While robo-advisors are an excellent tool, sometimes it takes a human perspective to touch on points that could be overlooked.

Financial Details

When you’re talking about a financial advisor service, you can’t overlook the financial details involved. Vanguard requires a minimum account deposit of $50,000. The fees you’ll find at Vanguard are as follows:

- 30% personal advisory fee

- Undisclosed transaction fees (re; hidden fees)

- Order fees with third-party mutual funds

Vanguard’s fees add up quickly. This means that while the fee schedule may seem competitive, but, in the long run it may not be.

An In-Depth Look at Wealthfront

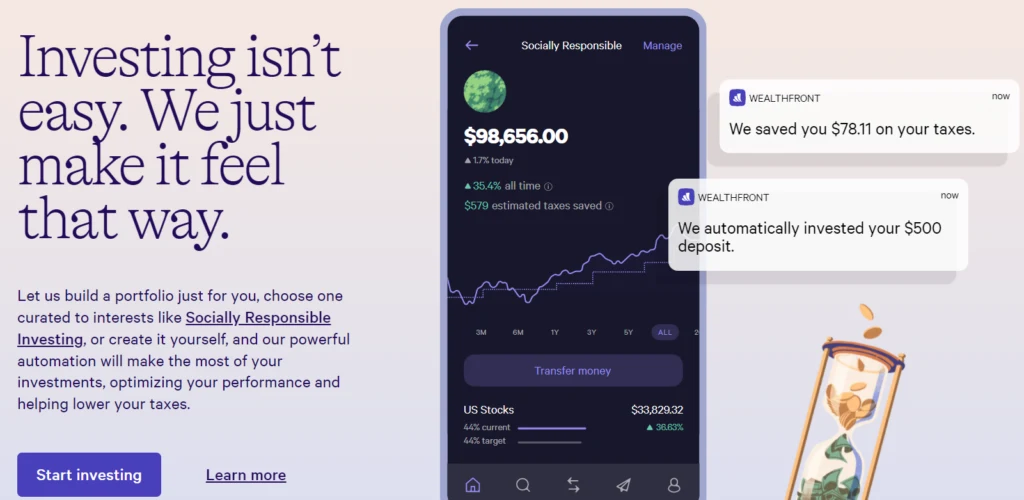

Of the two services being compared, Wealthfront is on the forefront of technology. The company’s main goal is to make financial education accessible to all. They have created what may be the most impressive robo-advisor available. It allows for little to no human contact, meaning that their clients can be hands-off with their accounts. With an entire software suite being developed for financial advising, Wealthfront has plenty to offer their clients.

Goal Setting Services

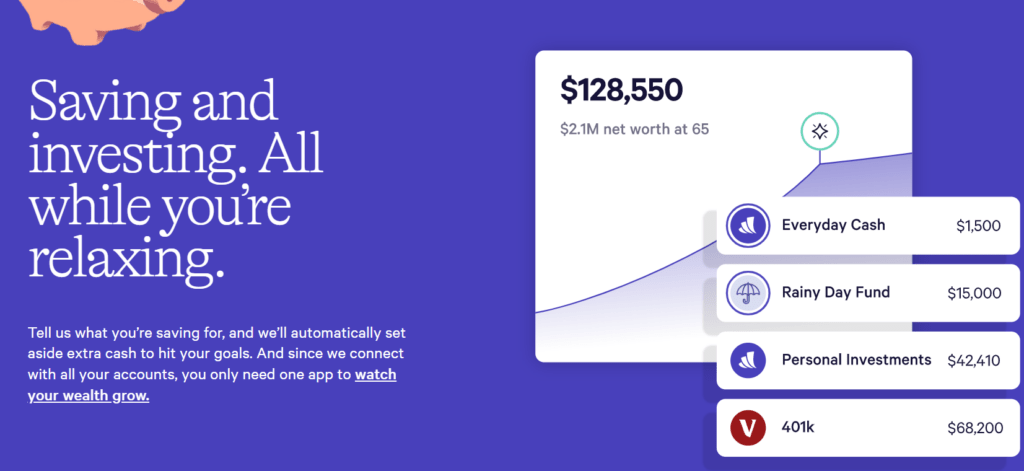

Wealthfront was designed with goal setting in mind. Their suite of tools are a comprehensive way to handle your financial planning. From the dashboard, clients can view all of their assets and liabilities at a glance. This gives a quick look at how your financial goals are being handled, and whether or not they’ll be met.

The Wealthfront account itself integrates with Redfin. This allows homeowners to review private schooling costs close to home, as well as in their desired neighborhoods. All college savings plans can be linked to U.S. universities, allowing expenses to be projected. These projections go beyond tuition, though. They also look at things like room and board, as well as books and other expenses.

Other real-world goal setting services include sabbatical planning, wedding planning, and automotive finance costs. These are just a few of the applications of the tools, with countless others available, as well.

Retirement Planning Services

Wealthfront’s robo-advisor is able to estimate net worth at retirement based on your financial state currently. It also lets you know how much you can comfortably spend per month once you are retired.

The planning tool for retirement, called Path, can help you compare projected retirement versus current spending habits, as well. This gives clients an idea as to whether or not their lifestyle can be maintained during retirement. Many inputs can be changed to manipulate the outcomes, like age of retirement, savings, target retirement spending, and life expectancy. Nothing is left to chance with Wealthfront’s retirement planning tools.

Account Types Offered

When comparing Wealthfront to Vanguard, you’ll find that Wealthfront offers a few more account types than their competitor. These account types are listed below:

- Individual, joint, and trust taxable accounts

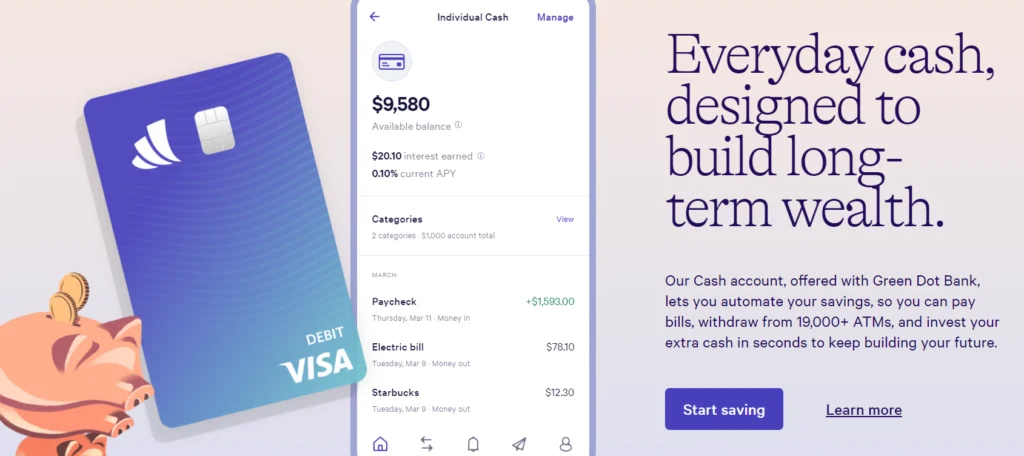

- Individual, joint, and trust high-interest cash accounts

- Traditional IRA accounts

- Roth IRA accounts

- SEP IRA accounts

- IRA transfer accounts

- 401(k) rollover accounts

- 529 college savings plan accounts

With Wealthfront offering college savings accounts, it’s a bit surprising that they don’t offer a couple of custodial accounts. These accounts are known as Uniform Gift to Minors Act (UGMA) or Uniform Transfer to Minors Act (UTMA) accounts. However, Vanguard does not offer these accounts either.

Features Offered to Clients by Wealthfront

This is the area in which Wealthfront tends to shine, and the audiences for these robo-advisors are split. Wealthfront is aimed towards younger clients, and younger clients tend to be more comfortable with technology. As such, the features you’ll find are a bit varied from what Vanguard offers.

The biggest feature for the younger crowd is the 529 college savings plan. This is a rare feature, exclusive to Wealthfront. The account itself reflects that rarity, though, coming with an administrative fee not found on all of the other accounts offered by Wealthfront. Wealthfront also offers a high-interest cash account, unlike their competitor.

Once your account at Wealthfront reaches $25,000, another feature is unlocked. This feature is the company’s portfolio line of credit. This line of credit is available at low interest rates to these higher-balance account holders at Wealthfront. There’s no credit check or credit score impact, and the line of credit is equal to 30% of your account’s value.

The final feature that sets Wealthfront apart is their PassivePlus investing feature. This feature is Wealthfront’s set of rule-based investment strategies, aimed to maximize client investments using tax-loss harvesting. The higher the value of the investments, the more PassivePlus strategies used. The more money you have with Wealthfront, the more money you’ll be able to make, in most cases.

Financial Details

Wealthfront has a minimum deposit amount of $500, making it accessible to nearly everyone. The fee structure posited by Wealthfront is easy to understand, as well. They charge a flat rate of 0.25% of your portfolio, assessed on a monthly basis. There are no fees charged for cash balances.

The ETFs that most portfolios are made up of tend to have annual management fees of 0.08%. Larger portfolios may be subject to investing in funds with slightly higher management fees, however.

The User Experience for Each Robo-Advisor

Vanguard

![]()

![]()

Vanguard is more of a hybrid service rather than a robo-advisor. The company provides human contact for advising on an appointment basis. If an appointment is not made, a human counterpart can still be reached, however. The company does not provide any form of chat support, though email can be used if you’re a part of the platform already.

Wealthfront

Wealthfront is a robo-advisor in the purest sense of the word. The company provides a customer support number for forgotten passwords, but that’s the extent of human contact. The Twitter account they have will occasionally answer questions, but it’s a long shot. If you need human contact in relation to your robo-advisor, you won’t find it with Wealthfront.

Breaking it Down

Pros of Vanguard

- A number of intuitive planning tools and calculators

- Hybrid support, with a robo-advisor and human advisors

- An onboarding process that integrates real-life scenarios with sterile planning scenarios

Cons of Vanguard

- High minimum deposit and high fees

- A lengthy onboarding process

- A lack of technological tools for planning

Pros of Wealthfront

- Low fees and low minimum deposit

- In-depth robo-advisor, and intuitive tools

- A variety of different account offerings not found elsewhere

Cons of Wealthfront

- No human support whatsoever

- Investing services are automated, which bodes poorly sometimes

FAQs

Answer: As discussed in this article, Vanguard is meant for high-net-worth investors who are already established. When investing at a minimum of $50,000, there are some expectations that come along with it. One of those is often a human advisor, offering assistance and explanations when necessary.

However, it can also be looked at in another light. Vanguard is also suitable for investors who aren’t the most technologically savvy. Adding the human element helps to bridge the gap between a technologically advanced robo-advisor and clients.

Answer: Wealthfront is designed for people who are just beginning to need financial tools to handle payroll services and more. The website has a low minimum account deposit, as well as low fees. For those just getting into the financial picture, Wealthfront may be a better option.

Additionally, this platform is best suited for people who are looking to take a hands-off approach. With technology and AI making all the decisions, you can sit back and watch the way things turn out. This is not for everyone, however. Thankfully, Wealthfront does it well.

Answer: With Wealthfront being entirely automated, many are concerned about online security on the platform. Wealthfront is a safe and secure website. As an additional security measure, Wealthfront allows users to enable two-factor authentication for all accounts, as well.

The Bottom Line

Unless you’re a high-net-worth investor, Wealthfront is the best option on the market when it comes to robo-advisories. The company allows for all of a client’s financial information to be accessible in one place. It also offers a variety of accounts not able to be found with other robo-advisors, like the 529 college savings plan and high-interest cash accounts. Unless you have the minimum $50,000 account deposit that Vanguard is asking for, it’s best to choose Wealthfront.

If you are a high-net-worth investor, though, Vanguard offers a suite of services and human advisors that may be of use to you. This hybrid system is designed with the established in mind. For more articles like this, be sure to visit Wallet on Fire!