- Strategic Capital vs Stone Street Capital: Who Should Buy Your Structured Settlement? - February 19, 2026

- The Best Financial Comparison Sites for Travel Credit Cards - January 17, 2026

- BestMoney.com Review: A CPA’s Perspective on a Financial Aggregator - January 15, 2026

I’ve spent years looking at the financial stacks of businesses and individuals, and whether I’m advising a construction firm on cash flow or helping a family optimize their tax strategy, the same principle always applies: You cannot manage what you do not measure. And you certainly cannot optimize what you do not compare.

In the last decade, we moved from walking into local bank branches to using direct online lenders, and now, we see the dominance of “aggregators” — platforms that do not lend money themselves but sit in the middle, connecting borrowers with banks.

One of the platforms making noise in this space is BestMoney.com.

I recently had a client ask me to take a serious look at this platform, wanting a walkthrough that cuts through the marketing. They wanted to know whether it was functional, safe, and actually useful for someone trying to secure capital or organize their budget.

So, I dug in. I reviewed the interface, the partner network, the loan terms, and the security protocols.

Here’s what I found.

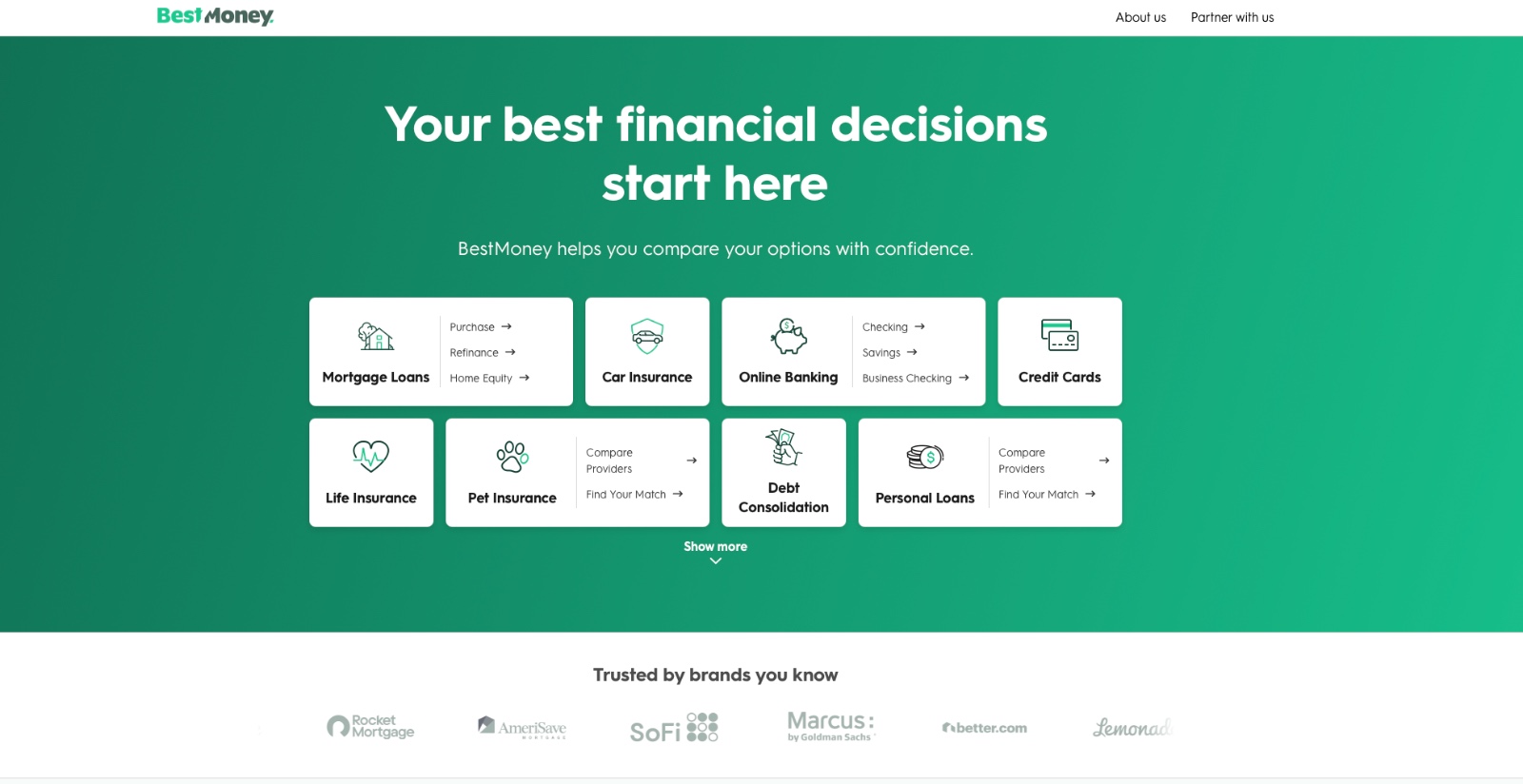

The 30,000-Foot View: What Is BestMoney.com?

BestMoney.com is not a bank or a lender; it is a financial marketplace comparison engine whose business model is lead generation.

When you enter your data into BestMoney, their algorithm filters through their partners (names like SoFi, LightStream, LendingClub, Rocket Mortgage) to find offers that match your credit profile and financial needs.

If you accept an offer, they hand you off to that lender to finish the paperwork, and the lender pays BestMoney a referral fee. That’s why BestMoney is free. You’re not the customer here; the lenders are.

This is a good thing because instead of filling out 15 different applications to see who gives you the best interest rate, you just fill out one form and get a consolidated list. As a CPA, this is a win in and of itself: If a tool saves you three hours of research, it’s already generated a return on investment (provided the data it gives you is accurate).

The Core Product: Personal Loans

The primary engine of BestMoney is their personal loan comparison tool. This is where most users enter the ecosystem.

What you need to first understand is that personal loans are a flexible financial tool. Unlike a mortgage (secured by a house) or an auto loan (secured by a car), personal loans are typically unsecured. This means the lender takes on more risk, which usually results in higher interest rates and often massive variance between lenders. For example, I’ve seen clients with a 720 credit score get quoted 8% by one bank and 14% by another — a spread that represents thousands of dollars in interest over the life of a loan.

This is where an aggregator like BestMoney proves its worth.

The Application Process

BestMoney avoids the pre-loan wall of text that plagues most financial sites. You start by selecting a loan purpose such as debt consolidation, home improvement, major purchase, etc.

It asks for the standard data points:

- Loan Amount: Covering a range from roughly $1,000 up to $100,000.

- Credit Score Estimate: Excellent, good, fair, poor

- Income and Employment Status: Crucial for debt-to-income (DTI) ratio calculations

One feature I appreciate here is their soft credit pull, which doesn’t affect your score. Instead of your score dropping by a few points after a hard pull, BestMoney allows you to window shop without damaging your credit profile.

The Rates and Terms

Because BestMoney is an aggregator, they do not set the shown rates. However, their partner network covers a wide spectrum.

- APR Ranges: I saw rates as low as roughly 5.99% for prime borrowers and ranging up to 35.99% for subprime borrowers.

- Loan Terms: Terms generally range from 24 to 84 months.

This 35.99% upper limit is high. That’s near credit card territory, so if you have poor credit, you need to be very careful. However, the lower end (~6%) is competitive with the best rates in the current market. The platform does a good job of presenting these clearly so you can compare the APR, not just the monthly payment.

Note: Always look at APR, not just the interest rate. APR includes the interest rate plus any origination fees and is the true cost of the loan.

Diversifying the Stack: Business Loans and Mortgages

While personal loans are their bread and butter, BestMoney has since expanded into business funding and mortgages.

Business Loans

BestMoney connects users to business lenders for things like working capital, equipment financing, and lines of credit.

The process is similar to the personal loan side, but the requirements are stricter. You’ll likely need to provide time-in-business and monthly revenue figures. Also, the partners here tend to be fintech lenders like BlueVine or OnDeck, rather than traditional SBA lenders.

These business loans are fast; you can often get funded in 24 to 48 hours. However, you definitely pay for that speed, and the effective interest rates on fast business capital can be significantly higher than a traditional bank loan.

That makes BestMoney a great tool if you need money now to seize an opportunity (like buying discounted inventory), but for long-term capital expenditure, you should compare these offers against your local bank.

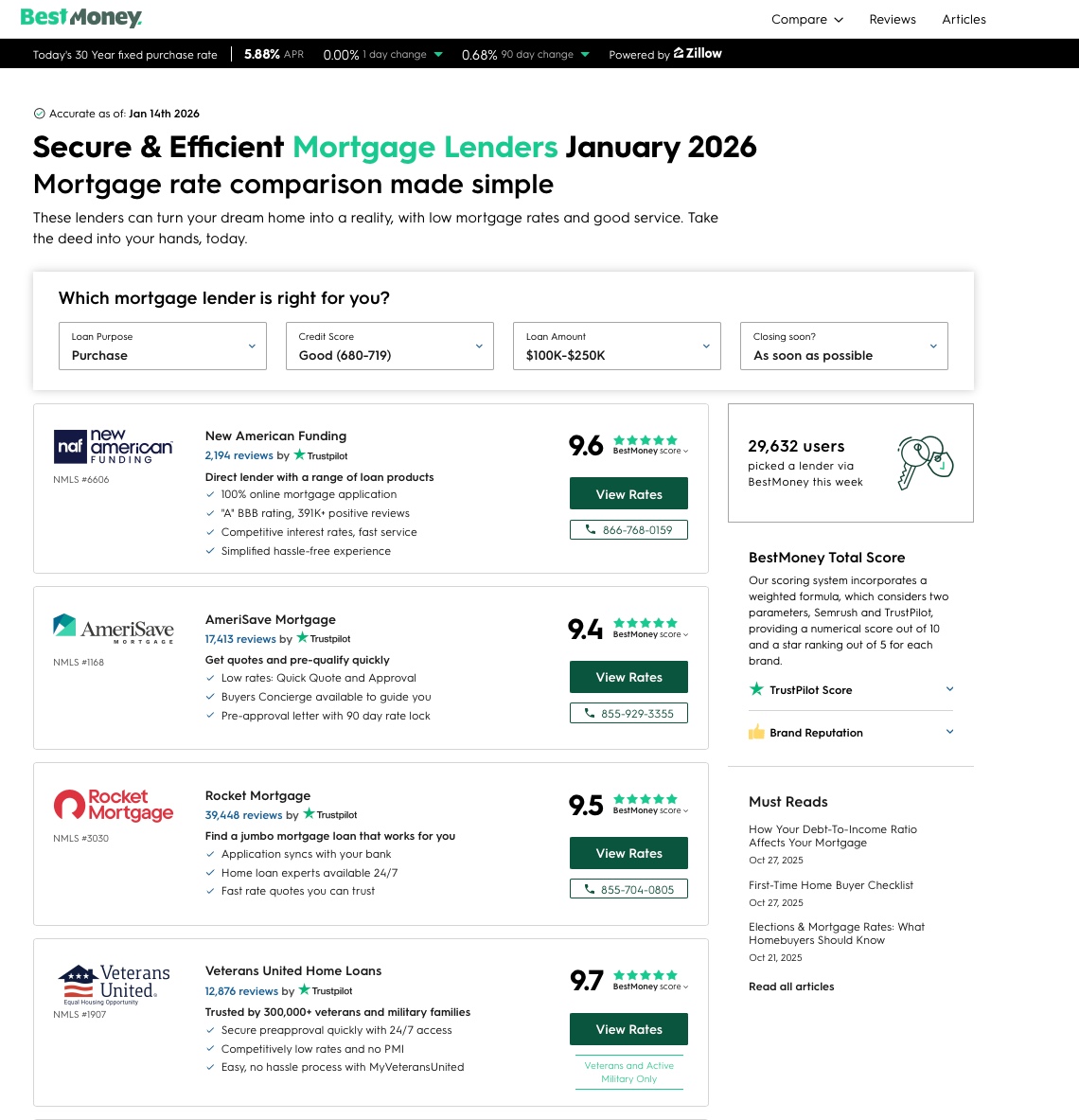

Mortgage Refinance and Purchase

BestMoney also offers a mortgage comparison vertical, connecting you with lenders for:

- New home purchases

- Refinancing

- Home equity loans (HELOANS) and lines of credit (HELOCs)

The interface here is robust and helps you calculate potential savings on a refinance. BestMoney simplifies the math by presenting partner offers side-by-side, showing the rate, the points (upfront fees to lower the rate), and the estimated monthly payment.

Safety and Security

Whenever you enter your Social Security number into a website, it’s easy to be paranoid — and you should be. Identity theft is a nightmare to unwind, which is why I also reviewed BestMoney’s security protocols.

The good news is that BestMoney uses the industry standard of 256-bit SSL encryption. This just means that when your data travels from your computer to their server, it’s scrambled. If a hacker intercepts it, all they get is a mess of random characters.

However, there’s no way to get around data-sharing here; because they’re a lead generator, their entire business model is built around sharing your information with lenders. You’re explicitly authorizing them to send your name, income, and SSN to their partners to get you a rate.

This means that if your data is sent to five lenders, you’re now in five different marketing databases. BestMoney is legitimate and secure, but you should expect an uptick in emails and phone calls from the partners they connect you with.

User Experience and Interface

I look at software all day, from QuickBooks to NetSuite. So I know what a good user experience should look like.

In my opinion, BestMoney is designed for the modern consumer.

- Mobile Optimization: I tested the site on my phone and my desktop, and it’s fully responsive. The sliders for selecting loan amounts work well with a thumb. The text is legible without pinching and zooming.

- Speed: The site loads fast. The “searching” animation it displays when it looks for partners is partly theatrical (just to show you it’s working), but the results appear quickly.

- Clarity: BestMoney uses simple and clear language. They don’t say “amortization schedule”; they say “monthly payment.” They explain terms with tooltips. This reduces the intimidation factor for people who aren’t finance professionals.

However, there is one downside to their aggregator model: Redirection.

When you click “See Deal” or “Apply,” you leave BestMoney.com and go to the lender’s site. The visual style changes. The navigation changes. This can be jarring for some users who think they are applying on BestMoney. So you have to be prepared to manage logins for different sites if you apply to multiple places.

The Pros and Cons

Let’s break this down into a simple list and see what makes sense and what doesn’t.

Pros:

- Efficiency: You get to see the market landscape in roughly two minutes. Doing this manually would take hours.

- Soft Credit Check: You can view rates without hurting your credit score.

- Education: The site does a good job of breaking down what the loans are for and what the terms mean.

- Breadth: They cover the full stack — loans, banking, mortgages, and then some. It’s a one-stop shop for comparison.

- Free for Users: The cost is borne by the lenders, not you.

Cons:

- Not a Direct Lender: BestMoney cannot approve you themselves; they can only introduce you. So if one of their partners rejects you, they can’t do anything about it.

- Marketing Volume: By submitting your info, you’re opting in to be contacted by lenders.

- Rate Variance: The teaser rates (e.g., “Rates starting at 5.99%”) are for perfect borrowers. If you have average credit, you’ll likely be disappointed by your rate if you don’t manage expectations.

Strategic Advice: How to Use BestMoney.com Effectively

As a CPA, here is how I would advise a client to use BestMoney in order to get maximum benefit with minimum hassle.

- Know Your Numbers First: Before you go to the site, know your current credit score (roughly) and your monthly income. Have a concrete number in mind for how much you need to borrow. Do not borrow “just in case”; borrow for a specific purpose.

- Use a Dedicated Email: If you are worried about marketing emails, create a free email address (like [email protected]) specifically for loan shopping. Use this for BestMoney and their partners so you can keep your primary inbox clean.

- Focus on the APR, not the Payment: Lenders can make a monthly payment look low by extending the term to five or seven years. However, this just means you pay massive amounts of interest. Look at the APR; that’s the true cost of the capital.

- Check the Origination Fee: Some lenders charge a fee just to process the loan (often 1% to 5% of the loan amount), which is usually deducted from the cash you receive. So if you need exactly $10,000 and there is a 5% fee, you might only receive $9,500. Make sure you account for this.

- Read the Pre-Payment Penalty Clause: I hate pre-payment penalties. If you come into some extra money and want to pay off your loan early to save on interest, you should be able to do so without a fine. Most modern online lenders have eliminated this fee, but always verify.

The Competitor Landscape

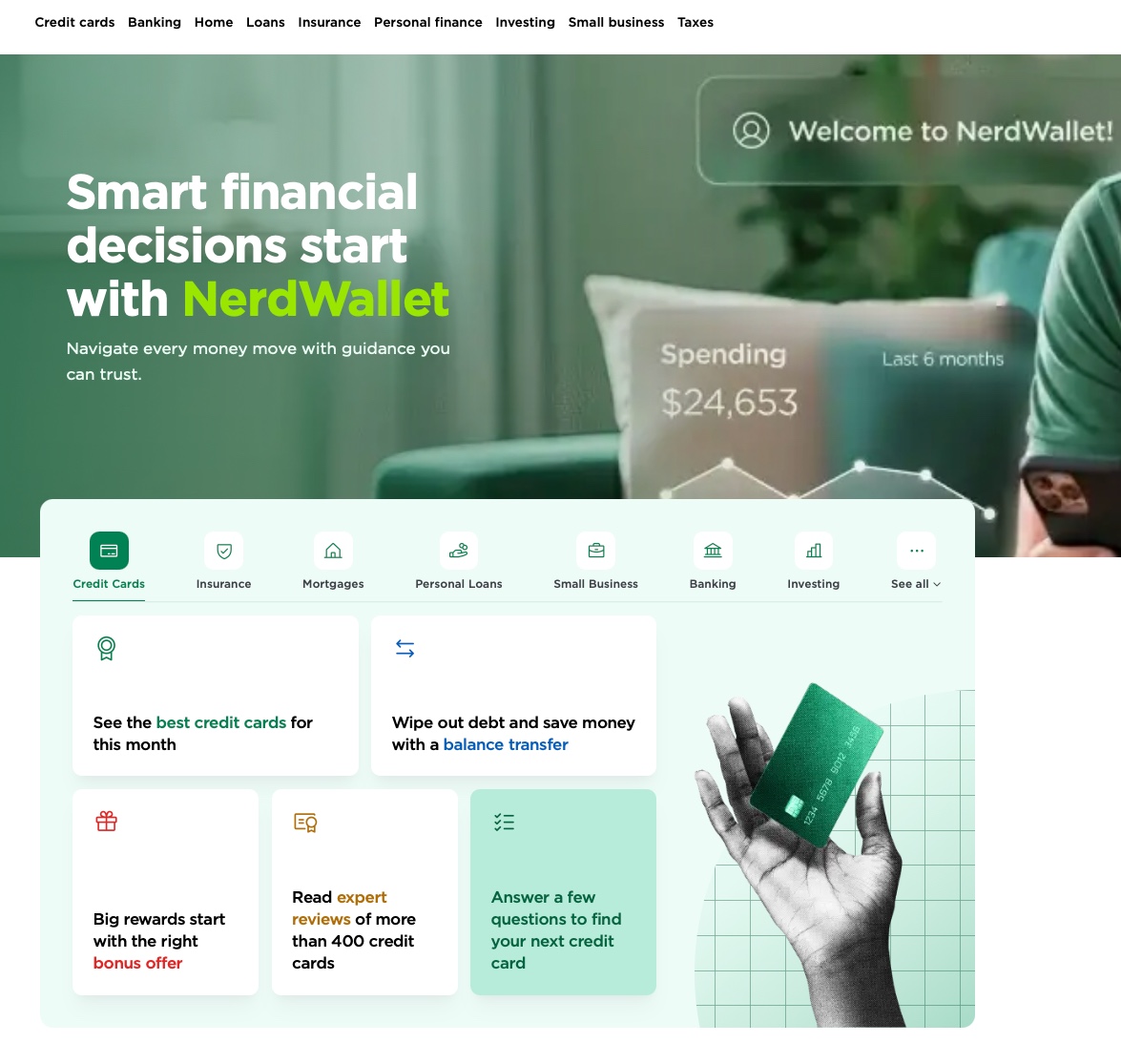

BestMoney is not the only player in town. You’ve likely heard of NerdWallet, Bankrate, and Credit Karma, and a review wouldn’t be complete without mentioning the other players in the space.

They’re all solid platforms that excel in their niches:

- NerdWallet is great for information; they write excellent articles and have similar comparison tools.

- Credit Karma is integrated into your credit report, so they use your actual credit data to suggest loans.

- Bankrate is very strong on the mortgage and banking side.

In my opinion, BestMoney differentiates itself by being very streamlined. It also feels less like a media company and more like a tool; if you want to read a dozen informational articles, go to NerdWallet. If you want to punch in numbers and get a list of lenders, BestMoney is a very direct, no-nonsense path to that data.

Final Verdict

Is BestMoney.com legit? Yes. Is it useful? Absolutely.

Most banks are counting on your laziness, assuming you won’t look elsewhere for a better rate. BestMoney.com is the antidote to that laziness tax; it forces lenders to compete for your business by putting the data in your hands.

If I were on the brink of any major financial decision, I’d at least use BestMoney as a part of the research phase. It’s a clean, secure, and highly functional utility for the modern borrower.

You don’t have to commit to anything; just go there, input your data, and see what the market says. If your local bank can beat these rates, great. If not, you have a digital path to cheaper capital.