- Renter Insurance Quote Comparisons: Finding the Best Coverage for Your New Home - February 16, 2026

- Which Pet Insurance Should I Get? How to Find the Best Plan - January 22, 2026

- Lease End vs. Swapalease: Which Is Better? - January 22, 2026

So, you want to save money on your healthcare expenses using a tax-advantaged spending account, but you’re not sure which one to go for.

Firstly, that’s pretty understandable. Deciphering the differences between an FSA (Flexible Spending Account) and an HSA (Health Savings Account) is difficult, as the two share a lot of similarities. Both offer tax-advantaged ways to pay for medical expenses, and there’s a huge degree of overlap in terms of the goods that qualify for each scheme.

However, there are important nuances between them in terms of how you lodge and grow your money. These nuances have a significant impact on the value you can access through your account.

How Do FSAs Work?

An FSA is typically offered through an employer, allowing you to set aside pre-tax dollars for qualified medical expenses. You set up the account through your company, and your contributions are deducted from your paychecks.

FSAs aren’t subject to any form of means test, meaning pretty much anyone can get one as long as their employer participates.

The big drawback here is that FSA funds expire at the end of the plan year (though some employers offer a brief grace period or a limited rollover at the end of the 12 months, usually capped at an additional 3 months). It’s a “use it or lose it” situation; if you don’t spend your money before the deadline, it’s gone.

This situation is made more complicated by the way in which you lodge your funds. You need to commit to a given monthly lodgement at the start of the year; if you think you’ll need, say, $300 per month to spend on qualifying items, you need to nominate this at the start of the year and stick to it. If you overshoot this number, you’ll either end up scrambling to spend excess money at the end of the year or else just letting it go to waste.

Plus, because FSAs are employer-administered, you may lose your account if you switch jobs in the middle of the year. There are some workarounds here, but keeping your money in this situation can be difficult.

How Do HSAs Work?

HSAs, on the other hand, offer a lot more flexibility when it comes to managing your money. They’re not tied to company plans, and there’s no time limit in terms of spending. You can roll funds over from one year to the next indefinitely. Your account isn’t tied to your job, so if you leave your current employer, your HSA will not be affected.

That’s not all; you can also put your account funds into investments, such as stocks or fixed-income securities. This isn’t possible under the FSA scheme. Plus, HSAs generally have higher contribution limits than FSAs.

There’s a catch, though. HSAs are available only if you’re enrolled in a high-deductible health plan (HDHP). These plans require you to pay a big chunk of money ($1,650 for an individual plan and $3,300 for a family plan) out of your own pocket when you submit a health insurance claim.

Unless you’re a young, single person in consistently good health, there’s a good chance that the benefits of having a HSA will be outweighed by the drawbacks of being stuck with a HDHP. This is a complex financial decision that will require you to take a detailed look at your own income and expenses, as well as your comfort level when it comes to healthcare coverage.

Spending Your Money

The other key differentiator between the two programs comes in terms of the goods you can purchase under each one.

When researching this article, I used FSA Store and HSA Store (sister stores that cater to each scheme specifically and exclusively) to compare the product ranges on offer. Both platforms offer only goods that are eligible for reductions under each scheme, so you know that everything you’re buying is deductible. Additionally, each store allows you to use your FSA or HSA debit card at the checkout, eliminating the friction that can come with declaring expenses if you use your ordinary credit card and claim back your savings later.

I’ve broken down the options by product category below.

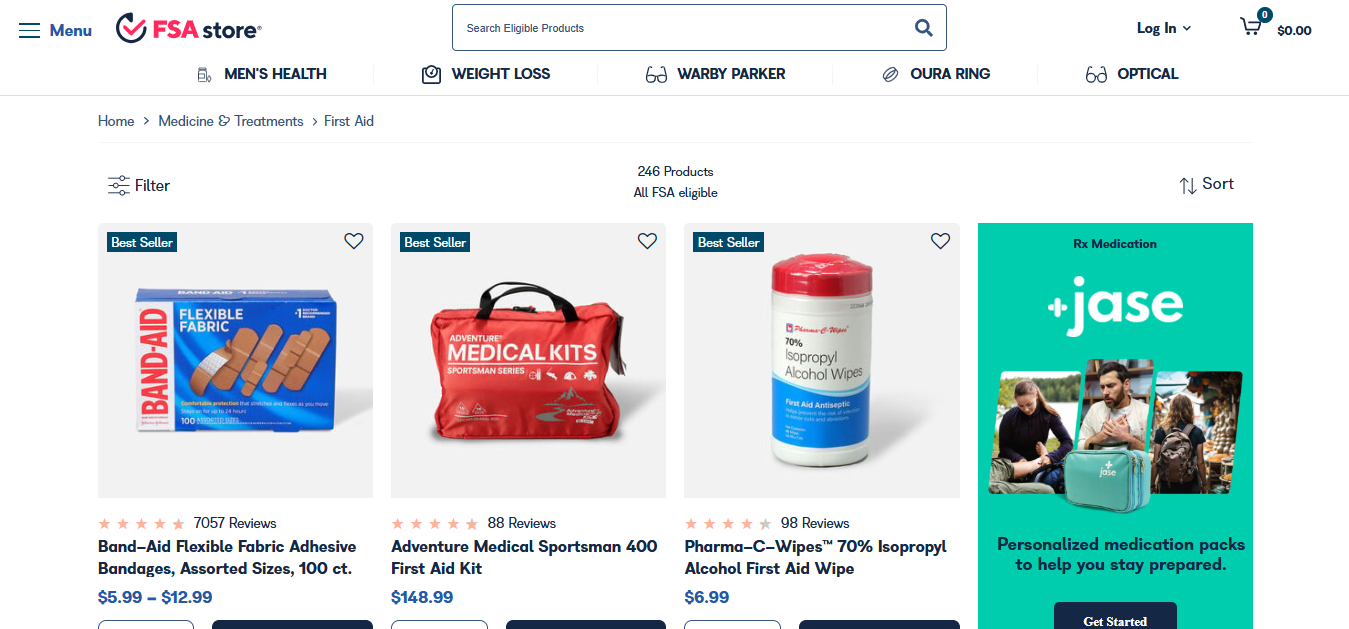

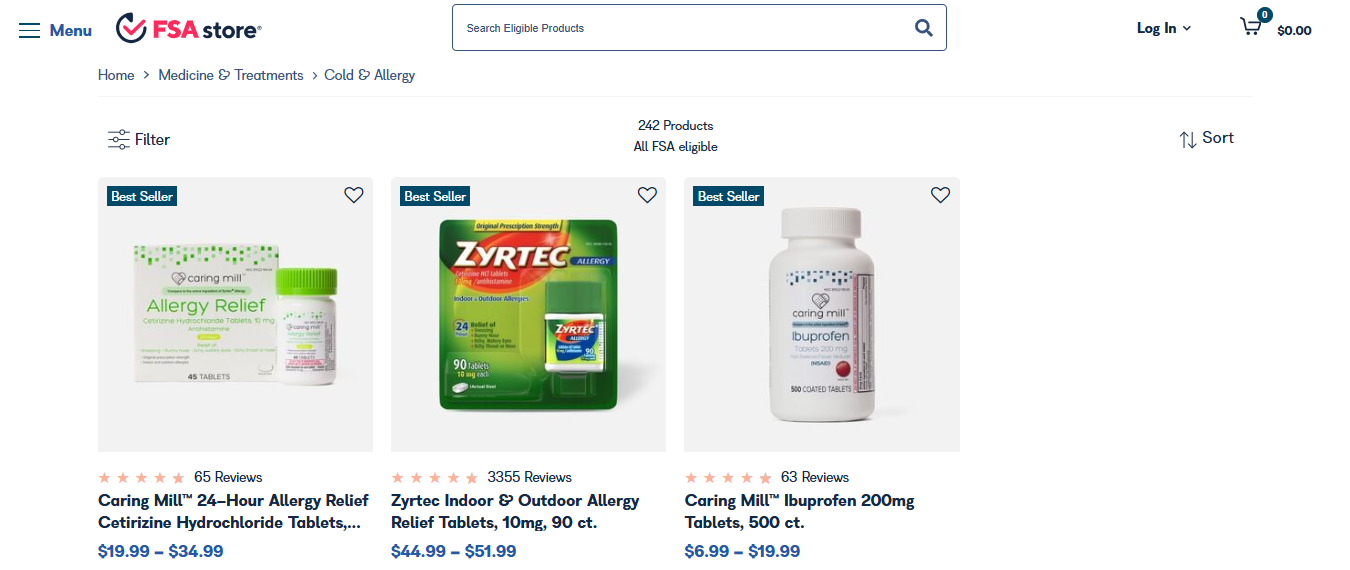

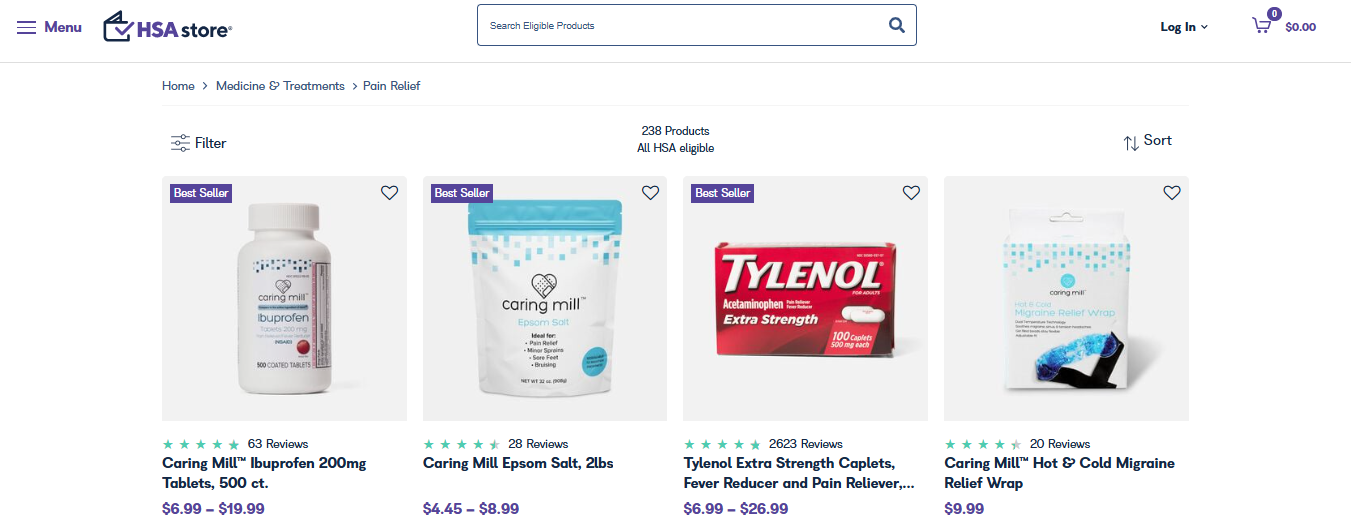

Medication & First-Aid Supplies

Both FSAs and HSAs offer expansive coverage in this category. Since the CARES Act introduced coverage for over-the-counter (OTC) medications without a prescription, the product ranges here are now massive and very useful for everyday needs.

Through FSA Store, I found an extensive lineup of first-aid supplies, ranging from basic adhesive bandages and antiseptic sprays to cold packs and wound care kits. There’s even a thoughtful curation of travel and emergency kits.

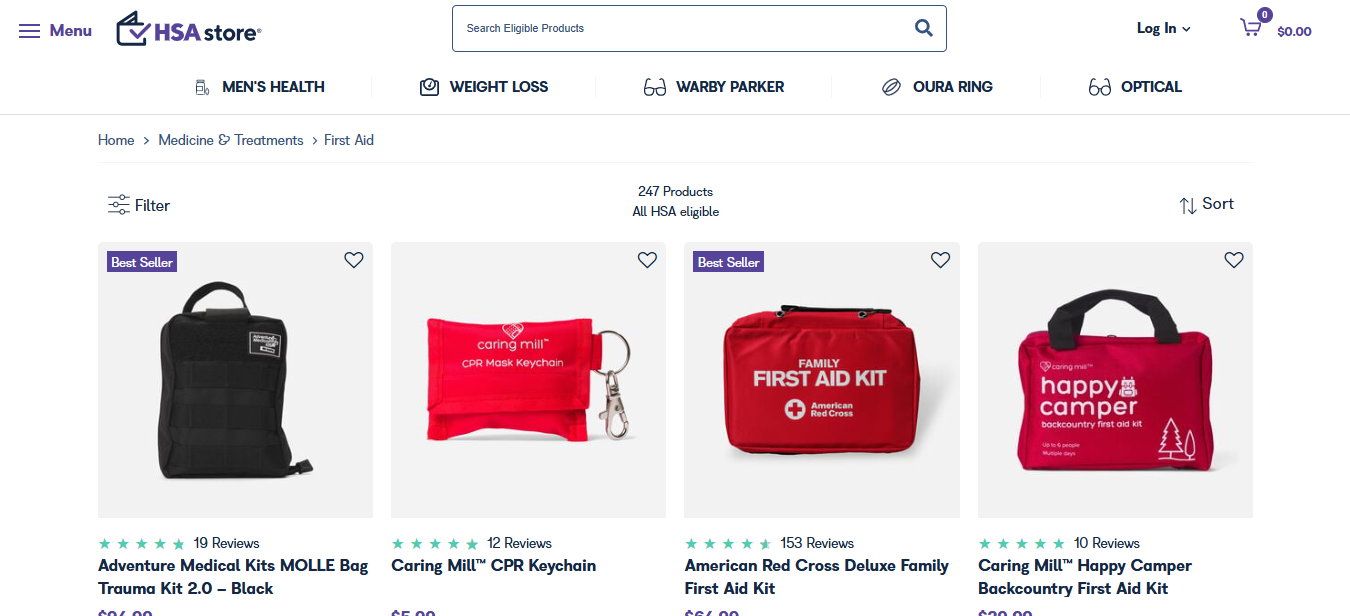

HSA Store mirrors much of the same inventory, but I noticed a slightly wider array of high-end OTC medications and specialty items like topical anesthetics, anti-itch gels, and sinus relief sprays. They also stock more in the way of cold and flu bundles, including thermometers, cough suppressants, and hydration tablets.

Both accounts cover the essentials well, but HSA Store offers a slightly broader and deeper selection.

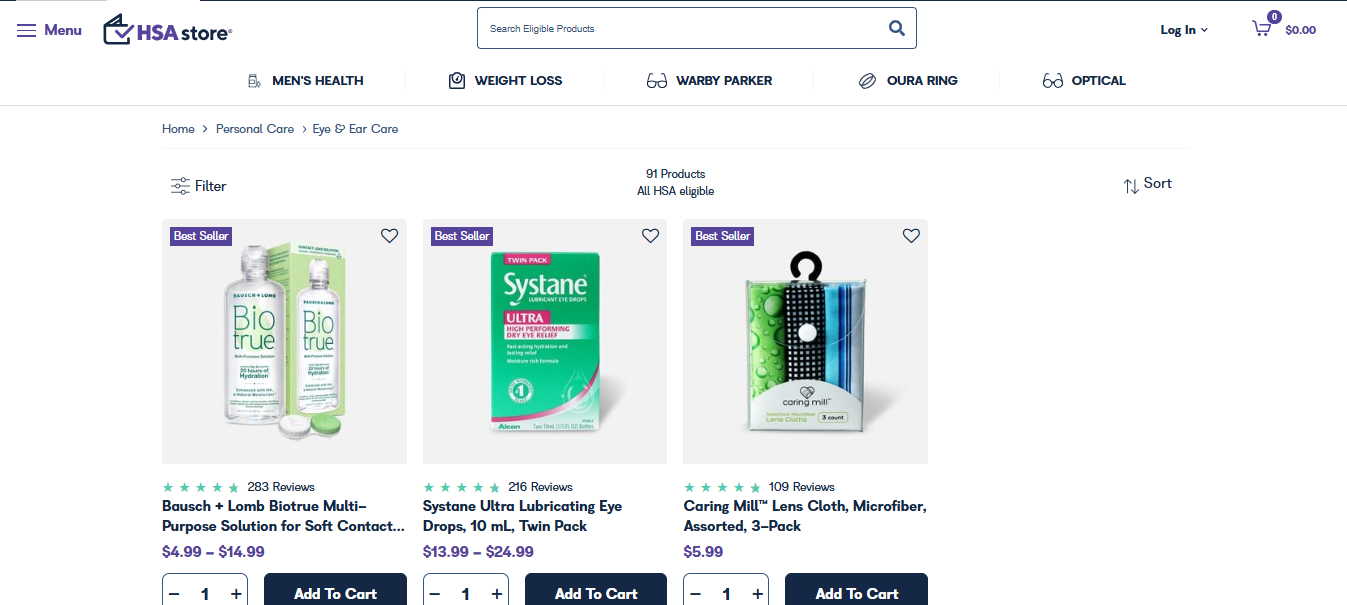

Vision & Eye Health

FSA Store does an excellent job covering the basics: contact lens solution, lens cases, lubricating eye drops, and even fashionable blue-light-blocking glasses. There’s also a wide range of designer frames on offer, which you can access with a prescription. You can even get prescription sunglasses; again, there’s a great selection of high-end brands to pick from.

HSA Store, however, goes a step further. In addition to all of the standard eye-care products, they also stock more specialized tools like punctal plugs, ocular vitamins, and premium-grade lens cleaning systems. Their selection of blue-light glasses includes designer-level options with anti-reflective coatings and frames tailored for all-day wear.

While FSA Store is more than adequate for regular eye-care needs, HSA Store offers a more robust inventory.

Hearing Aids & Accessories

FSA Store offers all the basics you need in this category: hearing aid batteries, cleaning kits, dehumidifiers, and wax guards. The platform also offers a great range of hearing aids, including Bluetooth-enabled models from the likes of Bose and HP.

HSA Store offers many of the same items, although there is a slightly broader selection on offer here. However, I would stress that you’ll probably find everything you need under either scheme.

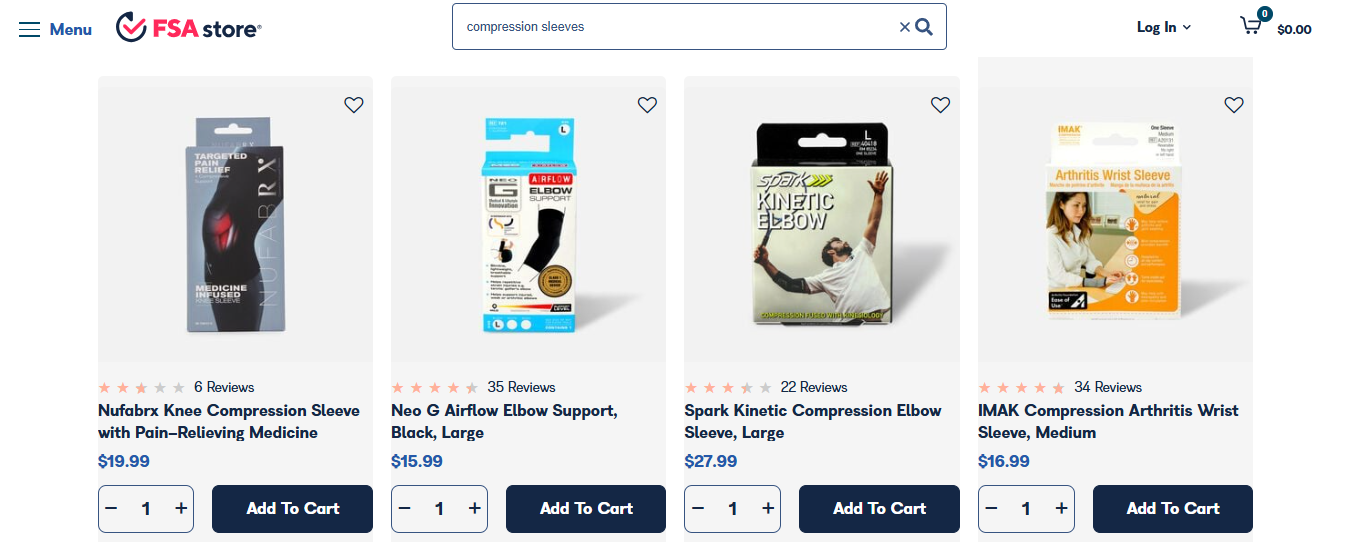

Orthopedic & Support Gear

FSA Store carries a decent variety of compression sleeves, wrist braces, and back supports. You’ll also find ice therapy wraps and posture-correcting gear. Their inventory caters well to musculoskeletal complaints of most types, even more severe issues.

The selection on HSA Store in this category is slightly narrower, but it still covers all the bases pretty well. As was the case in the last category, there’s really not much to separate the two stores here.

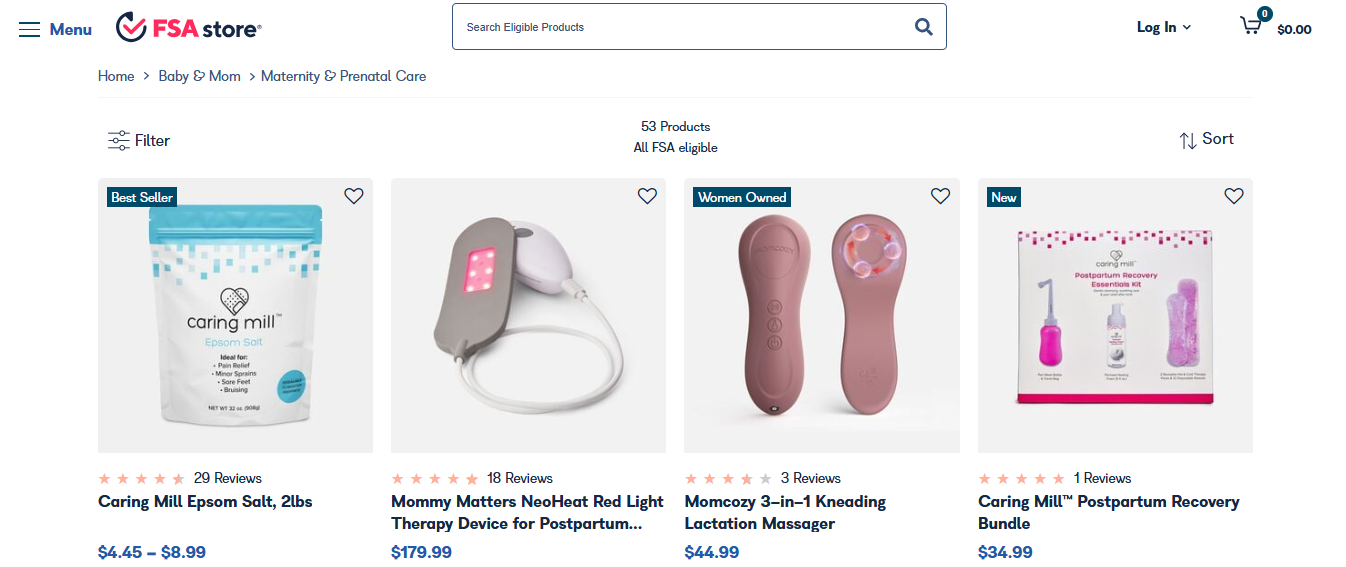

Baby & Pregnancy

Firstly, I would say that both schemes are incredibly helpful for new parents. Having a kid (or multiple kids) is an expensive game, so you’ll want to try to make savings wherever you can. It would be wise to take as much advantage of your FSA or HSA account as you possibly can here.

FSA Store offers breast pumps, prenatal vitamins, baby thermometers, nasal aspirators, and some nursing accessories. The selection is thoughtfully curated and perfect for meeting standard family planning needs.

This is the first category in which HSA struggles to keep up. It has a narrower selection to choose from in almost every subcategory. Still, though, you’ll find what you need here.

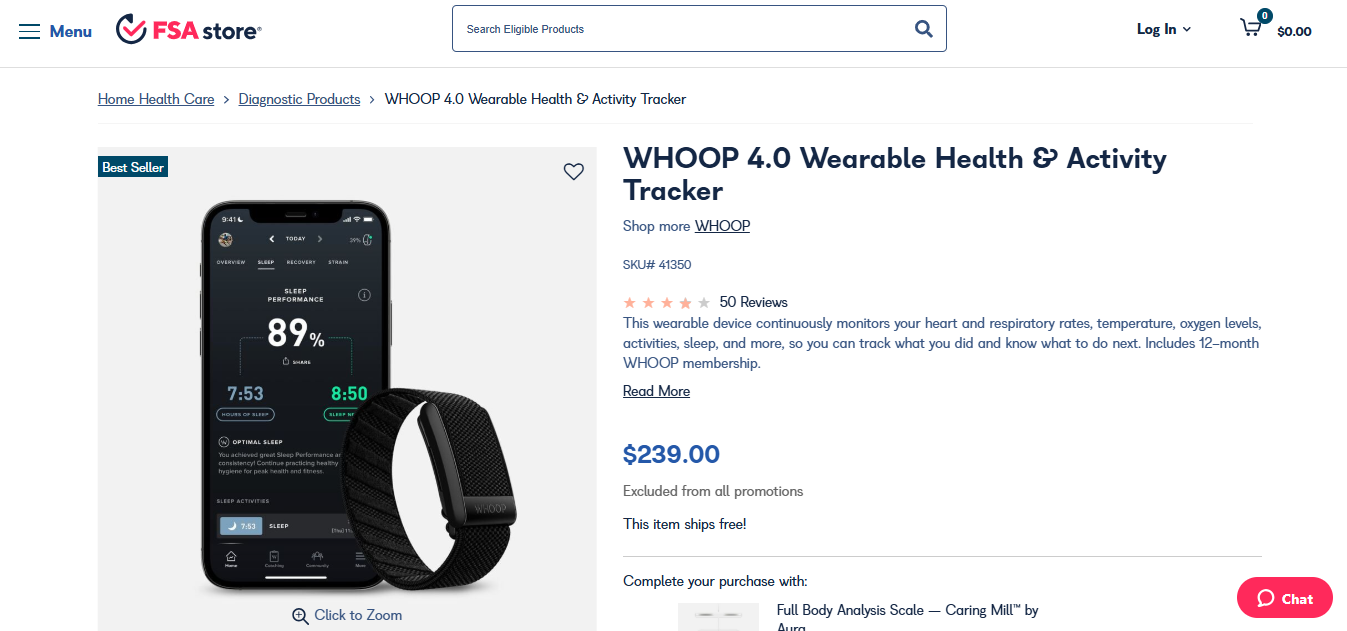

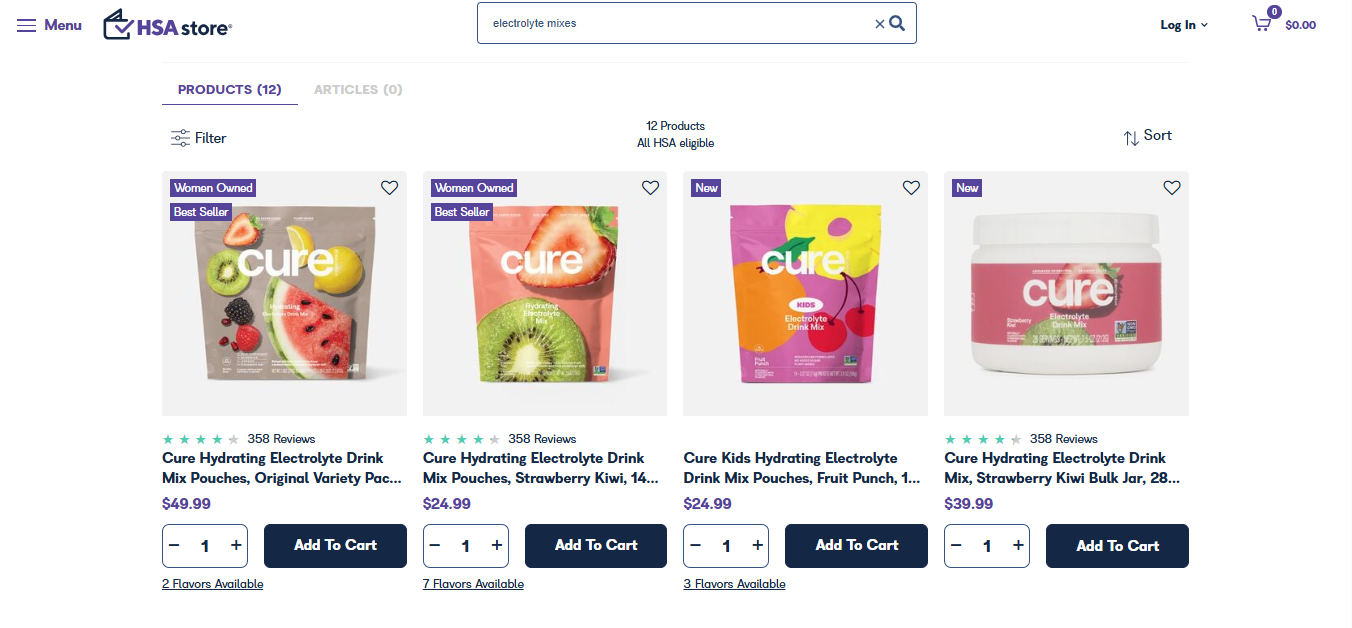

Fitness & Wellness

FSA Store’s fitness category offers a lot of unexpected options. You’ll find the likes of Whoop bands, post-partum belly wrap, and even electrolyte mixes. If you’re into sport or you’re just generally active, there’s a lot to like about what’s on offer here.

The HSA scheme offers a lot of the same items, but there are slightly fewer options to pick from. Again, though, I wouldn’t make the FSA vs. HSA decision solely on this basis; you’ll still be able to get pretty much whatever you need with a HSA.

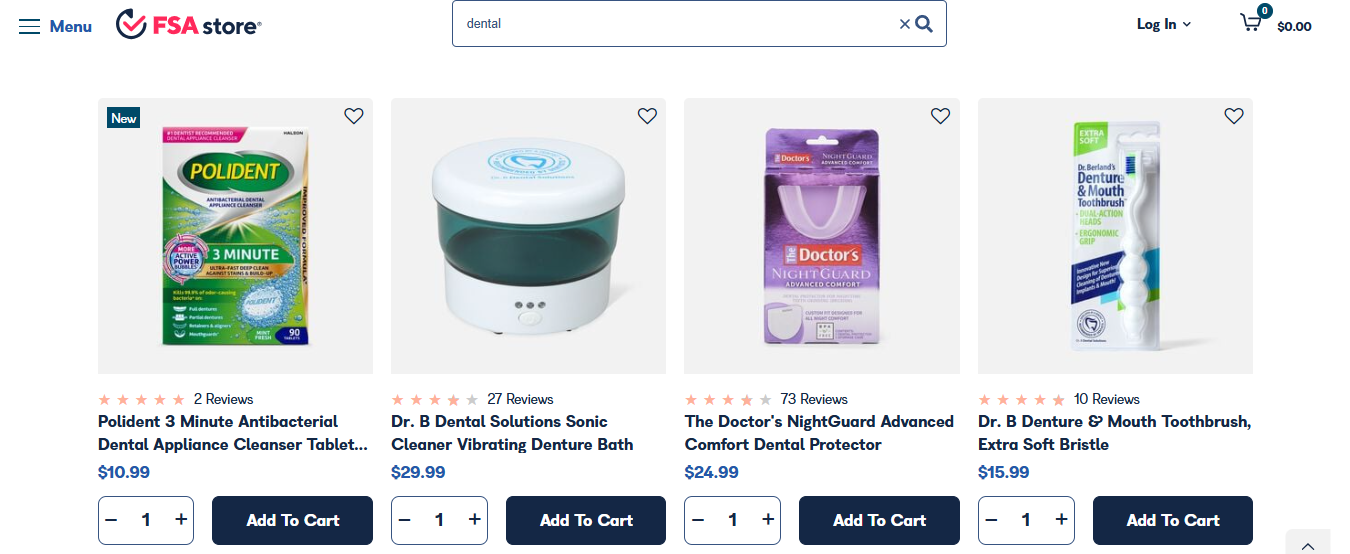

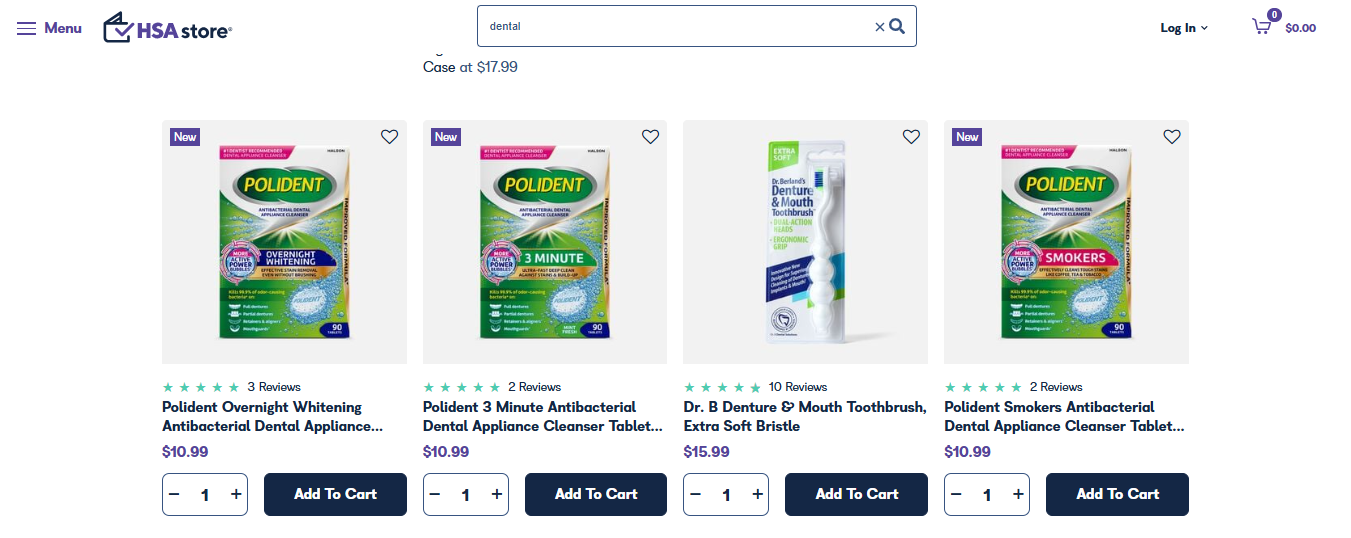

Dental Supplies

Dental care is well-supported under both FSAs and HSAs. FSA Store provides emergency dental kits, flossers, fluoride treatments, and bite guards. It’s a solid selection, particularly for travelers.

HSA Store includes all of that, but also has a slightly better selection when it comes to dentist-grade tools and home orthodontic kits.

FSA vs HSA: What’s the Verdict?

The selection of products across the board is probably slightly better under the HSA scheme, but not by much. Also, as I outlined above, this depends largely on what you’ll be spending your money on. HSA wins in some categories, FSA wins in others. I wouldn’t lose too much sleep over the differences here.

The real factor you need to consider is the way in which the plans are structured. The HSA system allows you to save money much more comfortably and even earn interest on the amount you leave in your account.

So, all other things being equal, HSA may seem like the better choice.

However, all other things are not equal.

In order to qualify for a HSA, you’ll need to use a HDHP, and this trade-off simply isn’t worth it in my opinion. If you end up needing to make a claim, all the savings you’ve made from your HSA vs. an FSA will evaporate instantly.

If you’re young and healthy, you might justifiably decide that the trade-off is worth it. However, for most categories of people (especially those who have health complaints or children), I think the FSA scheme is the better choice.

You still get great opportunities to save money, and you’re not restricted in terms of your access to effective health insurance.

If you have access to both types of accounts (this is only the case for a very limited number of people), your strategy should align with your needs. Use your FSA for immediate essentials, and let your HSA grow while using it for more strategic, long-term purchases.